Financeville CraigScottCapital is an online financial platform that has gained attention among investors in recent years. It is often presented as a company offering investment and trading services. Many people come across it while searching for ways to grow their money. However, there is limited clear information available about its background. This makes it important to understand what it actually offers.

The platform claims to provide opportunities in different financial markets. These may include forex trading, stocks, or other investment options. Some users are attracted by promises of high returns and easy profits. At the same time, others raise concerns about its transparency and operations. Because of this, investors should stay careful and informed.

Before investing in Financeville CraigScottCapital, it is important to do proper research. Check reviews, verify company details, and look for official registration. Many similar platforms exist, but not all are reliable. A clear understanding can help you avoid risks. Smart decisions always come from good knowledge and careful analysis.

Overview of Craig Scott Capital

Company Background

Craig Scott Capital was a New York-based broker-dealer firm that operated within the United States financial markets as a registered member of the Financial Industry Regulatory Authority, commonly known as FINRA. The firm presented itself as a full-service brokerage offering investment products and financial services to retail and institutional clients alike. At its operational peak, Craig Scott Capital employed a number of registered representatives and brokers who worked to manage client portfolios and facilitate securities transactions across various market segments.

The firm was founded with the stated intention of providing accessible investment opportunities to a broad range of clients, including retail investors who might not have had access to more exclusive financial institutions. It positioned itself as a nimble, client-focused brokerage that could compete with larger established players by offering personalized service and aggressive growth strategies. However, the internal practices of the firm would ultimately prove to be far removed from this client-centric presentation, and the gap between the firm’s public image and its actual operations became the central issue that regulators would eventually act upon decisively.

Craig Scott Capital’s business model relied heavily on the promotion of specific securities to retail clients, and the firm developed a reputation in certain financial circles for aggressive sales tactics that prioritized the firm’s own interests over the financial wellbeing of the clients it was supposed to serve. This fundamental conflict of interest, combined with the specific regulatory violations that were later documented and proven, ultimately led to consequences that would permanently remove the firm from the legitimate financial marketplace.

Recent Developments

The most significant recent development in the Craig Scott Capital story is its complete expulsion from FINRA, which represents the most severe disciplinary action that the regulatory body can take against a member firm. Following a detailed investigation and formal proceedings, FINRA concluded that Craig Scott Capital had engaged in conduct so fundamentally contrary to investor protection standards that its continued operation as a registered broker-dealer could not be permitted. The expulsion effectively ended the firm’s ability to operate as a legitimate financial services provider within the regulated United States markets.

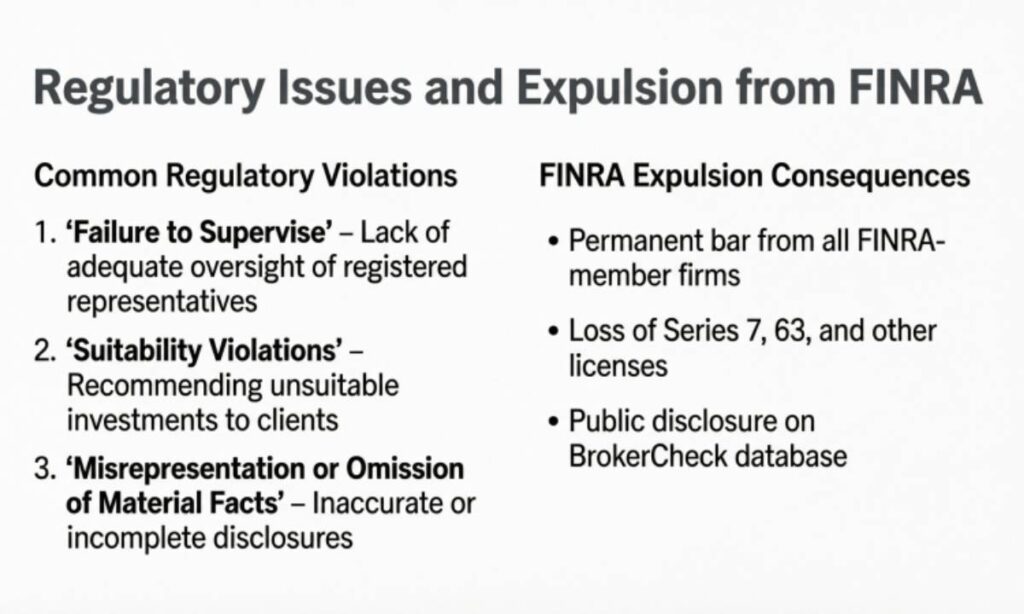

Regulatory Issues and Expulsion from FINRA

Reasons for Expulsion

The expulsion of Craig Scott Capital from FINRA was the culmination of regulatory findings that painted a deeply troubling picture of how the firm operated on behalf of its clients. FINRA’s investigation determined that the firm had engaged in systematic misconduct that violated multiple foundational rules designed to protect investors and maintain the integrity of the financial markets. These violations were not isolated incidents or administrative oversights — they reflected patterns of behavior that indicated deliberate choices to prioritize firm profits over client welfare.

- Churning of client accounts — executing excessive trades to generate commissions regardless of whether those trades benefited clients

- Unauthorized trading — executing transactions in client accounts without proper authorization from account holders

- Unsuitable investment recommendations — placing clients in investment products that did not match their stated risk tolerance or financial goals

- Failure to supervise — allowing registered representatives to engage in misconduct without adequate oversight from management

- Market manipulation — participating in schemes designed to artificially inflate the prices of certain securities

- Pump-and-dump activity — promoting securities to clients in order to benefit positions held by the firm or its associates

- Misleading communications — providing clients and regulators with inaccurate or incomplete information

- Failure to maintain required financial records in accordance with regulatory standards

Each of these violations, individually, would represent a serious breach of the standards that FINRA enforces to protect the investing public. Taken together, they demonstrated that Craig Scott Capital operated in a manner that was fundamentally incompatible with the principles of investor protection that are the foundation of regulated financial services. The expulsion was not simply a punishment — it was a necessary protective measure to prevent further harm to the retail investors who might otherwise have continued to be targeted by the firm’s practices.

| Violation Category | Description | Impact on Investors |

| Churning | Excessive trading to generate commissions | Unnecessary losses and fees |

| Unauthorized Trading | Trades made without client consent | Unwanted positions and losses |

| Unsuitable Recommendations | Wrong products for client risk profile | Portfolio misalignment and losses |

| Failure to Supervise | No oversight of representative conduct | Unchecked misconduct at all levels |

| Market Manipulation | Artificial inflation of security prices | Inflated purchase prices for clients |

| Misleading Communications | False or incomplete disclosures | Uninformed investment decisions |

Understanding FINRA’s Role

FINRA, the Financial Industry Regulatory Authority, is the primary self-regulatory organization overseeing broker-dealers and their registered representatives in the United States. It operates under the supervision of the Securities and Exchange Commission and is responsible for writing and enforcing rules governing the ethical activities of all registered broker-dealer firms and their employees. FINRA’s mandate is fundamentally protective — it exists to ensure that markets operate with fairness and integrity and that investors are treated with honesty and transparency by the professionals they trust with their money.

The tools available to FINRA range from fines and suspensions to the most severe sanction of expulsion, which permanently bars a firm from FINRA membership and therefore from operating as a registered broker-dealer in the United States. When FINRA reaches the threshold of expulsion, it has determined that the violations committed are so serious and the risk of ongoing harm to investors is so significant that no lesser remedy is sufficient. Expulsion is reserved for the most egregious cases and represents the complete withdrawal of the privilege to operate within the regulated financial marketplace.

For retail investors, understanding FINRA’s role is essential for navigating the financial services landscape safely. FINRA maintains a publicly accessible database called BrokerCheck, which allows anyone to look up the registration status, employment history, and disciplinary record of any broker or brokerage firm that has ever been registered with FINRA. This tool is one of the most important resources available to investors conducting due diligence on a potential financial advisor or broker, and the case of Craig Scott Capital illustrates precisely why checking a firm’s regulatory history before entrusting it with your money can be a financially critical decision.

Navigating Financial Content in Financeville

The Shift to Financial Content

Financeville refers to the sprawling ecosystem of online financial content — websites, social media accounts, YouTube channels, podcasts, newsletters, and forums — that has grown exponentially alongside the democratization of investing. As retail participation in financial markets has increased, so has the volume of content purporting to offer investment advice, market analysis, stock picks, and financial education. This ecosystem ranges from genuinely valuable, professionally produced educational content to outright fraudulent schemes dressed up in the visual language of legitimate financial media.

The intersection of Financeville with firms like Craig Scott Capital is a cautionary story about how the lines between entertainment, education, and financial promotion can be deliberately blurred to exploit investors who may not have the experience to distinguish between them. Content that appears to be offering impartial market analysis may in reality be serving the interests of firms or individuals who hold positions in the securities being discussed. This form of undisclosed promotion is not only ethically problematic — in many cases it constitutes market manipulation under securities law.

Identifying Credible Financial Information

In a digital landscape saturated with financial content of wildly varying quality and integrity, the ability to identify credible sources of information is one of the most valuable skills any investor can develop. Credible financial content is characterized by transparency about the author’s credentials and potential conflicts of interest, clear sourcing of data and claims, acknowledgment of uncertainty and risk, and the absence of high-pressure urgency designed to prompt immediate action. Content that consistently meets these standards is the kind that genuinely serves investor interests.

- Look for authors or creators with verifiable professional credentials and regulatory registration

- Check whether content discloses any financial interests in the securities being discussed

- Prefer sources that acknowledge risk and downside scenarios alongside potential gains

- Be deeply skeptical of content that creates urgency, scarcity, or fear of missing out

- Cross-reference any specific investment recommendations with independent sources before acting

- Distinguish between entertainment-format financial content and genuinely analytical reporting

- Verify that any firm or individual offering financial services is registered with relevant regulators

Regulatory Concerns: What Investors Should Know

Common Red Flags

Regulatory concerns in the financial services industry tend to follow recognizable patterns, and investors who are familiar with the common warning signs of misconduct are significantly better positioned to protect themselves. The violations that led to Craig Scott Capital’s expulsion from FINRA are not unique — similar patterns of misconduct appear repeatedly across cases involving rogue brokers and brokerage firms throughout the industry’s history. Recognizing these patterns before money changes hands can prevent significant financial harm.

- Guarantees of high returns with little or no risk — all legitimate investments carry risk

- Pressure to invest quickly before an opportunity disappears

- Difficulty reaching your broker or getting clear answers about your account

- Account statements that are confusing, inconsistent, or hard to understand

- Unexpected trades appearing in your account that you did not authorize

- Recommendations that seem to prioritize the broker’s commission over your financial goals

- Reluctance to provide clear documentation of fees, commissions, and conflicts of interest

- Unusually high trading frequency in your account relative to your investment objectives

Importance of Due Diligence

Due diligence is not simply a best practice in investing — it is a fundamental responsibility that every investor carries for their own financial protection. No regulatory body, however well-funded and diligent, can fully substitute for the protective effect of investors who ask hard questions, verify credentials, read documents carefully, and refuse to be rushed into decisions. The case of Craig Scott Capital demonstrates what can happen when investors place excessive trust in a firm’s self-presentation without independently verifying its regulatory standing and track record.

| Due Diligence Step | Why It Matters | How to Do It |

| Check FINRA registration | Confirms firm is legally authorized | Use FINRA BrokerCheck database |

| Review disciplinary history | Reveals past violations and sanctions | FINRA BrokerCheck and SEC EDGAR |

| Verify credentials | Confirms claimed qualifications are real | Check licensing bodies directly |

| Read all documents | Ensures you understand fees and terms | Review account agreements carefully |

| Understand the fee structure | Prevents hidden cost surprises | Ask for full written fee disclosure |

| Monitor account activity | Detects unauthorized trading early | Review statements monthly |

| Seek second opinions | Provides independent perspective | Consult a fee-only fiduciary advisor |

The Crypto Angle: Craig Scott Capital’s Involvement

Cryptopia: Overview of Crypto-Related Content

The rise of cryptocurrency markets created new opportunities for the kind of promotional and manipulative activity that regulators have long fought in traditional securities markets. Craig Scott Capital’s involvement in cryptocurrency-adjacent activities reflects a broader trend of firms with questionable regulatory histories migrating toward crypto markets, which have historically operated with less regulatory oversight than traditional securities markets. The decentralized, pseudonymous nature of many cryptocurrency transactions makes them appealing to those seeking to conduct promotional schemes outside the reach of traditional market regulators.

Crypto-related financial content — sometimes grouped under terms like “Cryptopia” in online communities — encompasses an enormous range of material from genuinely educational blockchain explanations to outright fraudulent investment schemes. The challenge for investors navigating this space is that the visual and rhetorical markers that distinguish credible content from promotional manipulation in traditional finance are not always as well established in crypto communities. This makes the crypto content ecosystem a particularly fertile ground for the kind of misleading financial promotion that characterized Craig Scott Capital’s activities in the traditional markets.

Best Practices for Cryptocurrency Investments

Investors considering cryptocurrency exposure should apply due diligence standards that are at least as rigorous as those applied to traditional securities investments — and in many cases more rigorous, given the relative immaturity of regulatory frameworks in the crypto space. The absence of the regulatory protections that exist in traditional securities markets means that the burden of individual investor caution is correspondingly higher when dealing with crypto assets.

- Only invest what you can genuinely afford to lose entirely — crypto markets are highly volatile

- Research the underlying technology and use case of any cryptocurrency before investing

- Be extremely skeptical of influencers or content creators promoting specific crypto assets

- Understand that anonymous or pseudonymous project teams represent a significant red flag

- Use only regulated, licensed cryptocurrency exchanges with strong security track records

- Store significant crypto holdings in hardware wallets rather than on exchange platforms

- Never invest based solely on social media hype, viral trends, or celebrity endorsements

- Diversify crypto exposure rather than concentrating in a single asset or project

Assessing Trustworthiness

Should You Trust Financeville CraigScottCapital?

The direct answer to whether investors should trust Craig Scott Capital or content associated with it is unambiguous: the firm has been expelled from FINRA, the primary regulatory body overseeing broker-dealers in the United States, which represents the most severe finding of misconduct available under FINRA’s disciplinary framework. A firm that has been expelled from FINRA has had its authorization to operate as a registered broker-dealer completely revoked. Any continued financial activity conducted under the Craig Scott Capital name or brand following this expulsion would lack the regulatory authorization required for legitimate financial services provision in the United States.

Red Flags to Watch For

- Any entity claiming affiliation with or successor status to Craig Scott Capital

- Financial content that references Craig Scott Capital in a positive or promotional context

- Online communities or forums promoting securities associated with the firm’s history

- Social media accounts or content channels claiming special insight from former firm associates

- Investment newsletters or tipping services with connections to the firm’s former registered representatives

- Crypto or alternative investment projects promoted through channels linked to the firm

Impact on Retail Investors and Lessons Learned

The retail investors who trusted Craig Scott Capital with their savings and investments are the most important part of this story, and their experiences should serve as the central lesson that the financial community draws from the firm’s conduct and downfall. Retail investors — individuals who invest their personal savings rather than institutional or professional capital — are the participants in financial markets who are most vulnerable to misconduct because they typically have less experience, less access to independent research, and less legal and financial resource to pursue remedies when they are harmed.

The documented violations at Craig Scott Capital — churning, unauthorized trading, unsuitable recommendations, and market manipulation — are precisely the practices that most severely harm retail investors. These are not abstract regulatory technicalities. They represent real people who found their savings diminished by trading activity they did not authorize, who were placed in investments that were inappropriate for their financial situation, and who made decisions based on information that was designed to serve the interests of the firm rather than their own. The harm done to these individuals is concrete and in many cases irreversible.

- Never place all investment assets with a single broker or firm regardless of how trusted they seem

- Regularly review account statements and immediately flag any unauthorized or unexpected activity

- Understand every product you invest in before committing capital to it

- Recognize that commission-based compensation structures create conflicts of interest

- Know that you have the right to file complaints with FINRA, the SEC, and state regulators

- Seek the services of fee-only fiduciary advisors who are legally required to act in your interest

- Never allow a broker to take discretionary control of your account without full understanding

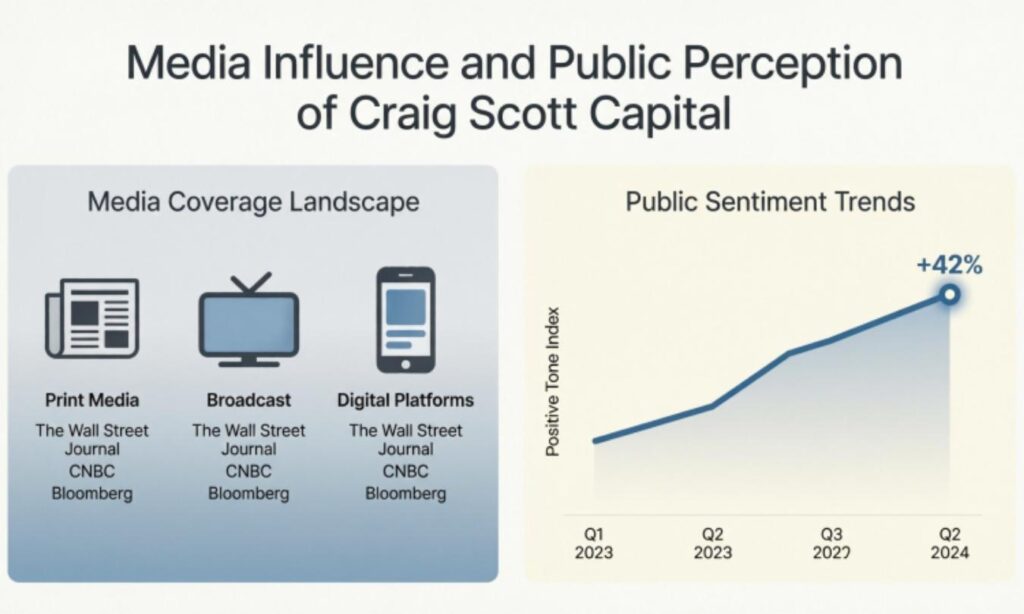

Media Influence and Public Perception of Craig Scott Capital

Media coverage plays a powerful role in shaping public perception of financial firms, and the Craig Scott Capital case illustrates both the positive and negative dimensions of that influence. On the negative side, firms like Craig Scott Capital have historically benefited from periods when their activities did not attract significant media scrutiny — operating in the relative darkness of low public awareness allows misconduct to continue longer than it otherwise might. The absence of coverage is not the same as the absence of wrongdoing, and investors who rely on media attention as a proxy for regulatory legitimacy are making a dangerous assumption.

On the positive side, investigative financial journalism and regulatory reporting have consistently played a crucial role in exposing misconduct that affects retail investors. Journalists who specialize in financial fraud, market manipulation, and broker misconduct provide an important layer of accountability that supplements formal regulatory action. The public exposure of Craig Scott Capital’s violations — through both regulatory proceedings and media coverage — serves a protective function by informing current and potential investors about the documented risks associated with the firm.

Social media has added a complex new dimension to the media landscape around financial firms. Online communities can rapidly spread both accurate warnings about fraudulent activity and misleading promotional content that serves the interests of bad actors. The challenge for investors is developing the media literacy to distinguish between these two types of content in real time, without the benefit of the slow verification processes that formal journalism and regulatory investigation employ.

Alternative Platforms: Where Can Investors Turn?

For investors who have experienced harm from firms like Craig Scott Capital, or who are simply looking to establish relationships with financial service providers they can trust, the landscape of legitimate alternatives is broad and well-regulated. The key distinction to seek is the fiduciary standard — a legal obligation that requires financial advisors to act in their clients’ best interest rather than simply recommending suitable products. Registered Investment Advisors are held to the fiduciary standard, unlike broker-dealers who are held only to a suitability standard, which is a meaningfully lower bar.

- Registered Investment Advisors registered with the SEC or state securities regulators

- Fee-only financial planners who charge flat fees rather than earning commissions on products

- FINRA-registered broker-dealers with clean disciplinary records verifiable through BrokerCheck

- Non-profit credit counseling organizations for debt management and basic financial planning

- Robo-advisor platforms regulated by the SEC offering low-cost diversified investment management

- Direct index investing services that provide broad market exposure at low cost

- Community development financial institutions for investors seeking socially oriented services

| Provider Type | Regulatory Standard | Best For | Cost Structure |

| Registered Investment Advisor | SEC / State fiduciary | Comprehensive financial planning | Fee-based or flat fee |

| Fee-Only Financial Planner | Fiduciary standard | Unbiased holistic advice | Hourly or retainer |

| FINRA Broker-Dealer (clean record) | Suitability standard | Securities transactions | Commission or fee |

| Robo-Advisor | SEC registered | Passive investment management | Low annual percentage |

| Credit Union Financial Services | NCUA regulated | Basic savings and lending | Member-based low cost |

Rebuilding Trust in a Post-Craig Scott Era

The financial services industry’s ability to rebuild trust with retail investors following high-profile cases of misconduct depends on several interconnected factors: stronger and more consistent regulatory enforcement, greater transparency in compensation structures and conflicts of interest, improved financial literacy among retail investors, and a cultural shift within the industry toward genuinely client-centered practice. Each of these factors requires sustained effort from regulators, industry participants, educators, and investors themselves.

Regulatory bodies like FINRA and the SEC have taken meaningful steps in recent years to strengthen investor protection frameworks, increase the transparency of broker compensation, and improve the accessibility of disciplinary records. The expansion of BrokerCheck and the implementation of Regulation Best Interest represent genuine progress, even if critics argue that these measures do not go far enough to eliminate the conflicts of interest that enable misconduct. The direction of travel in regulatory reform is positive, but the pace of change must continue to accelerate to keep up with the evolving tactics of bad actors in the marketplace.

For individual investors, rebuilding trust in financial services begins with the recognition that trust must be earned through verification rather than extended by default. The most empowered investor is one who understands their rights, knows how to verify the credentials and history of those who manage their money, and is equipped to recognize the warning signs of misconduct before harm occurs. The Craig Scott Capital case, for all the damage it caused, provides a clear and detailed illustration of what investor-harming misconduct looks like in practice — and that knowledge, applied proactively, is one of the most powerful tools available for protecting personal financial futures.

| Topic | Key Point |

| Company Status | Expelled from FINRA — no longer authorized as registered broker-dealer |

| Primary Violations | Churning, unauthorized trading, market manipulation, unsuitable recommendations |

| Investor Impact | Retail investors suffered financial losses through documented misconduct |

| Crypto Involvement | Promotional activity in less-regulated crypto markets noted |

| Red Flags | Guarantees of return, pressure tactics, unauthorized account activity |

| Due Diligence Tool | FINRA BrokerCheck for verifying registration and disciplinary history |

| Best Alternative | Fee-only fiduciary registered investment advisors |

| Regulatory Body | FINRA (self-regulatory) operating under SEC supervision |

| Lesson for Investors | Verify before you trust — regulatory records are publicly accessible |

Frequently Asked Question

What is Financeville CraigScottCapital?

Financeville CraigScottCapital is an online platform that claims to offer investment and trading services to users.

Is Financeville CraigScottCapital legit or a scam?

Its legitimacy is unclear, so investors should research carefully before trusting the platform.

How does Financeville CraigScottCapital work?

It reportedly allows users to invest money in different markets like forex or stocks for potential returns.

Can you make money with Financeville CraigScottCapital?

Some users claim profits, but there is no guaranteed return, and risks are involved.

Is Financeville CraigScottCapital safe to use?

Safety depends on its transparency and regulation, which should always be verified first.

What services does Financeville CraigScottCapital offer?

It may offer trading, investment plans, and financial management services.

Are there any reviews of Financeville CraigScottCapital?

Yes, reviews are mixed, with some positive experiences and some concerns reported online.

How to start investing in Financeville CraigScottCapital?

Users usually sign up, deposit funds, and choose an investment plan to begin.

Does Financeville CraigScottCapital require a minimum deposit?

Most platforms like this have a minimum deposit, but exact details should be confirmed.

Why is Financeville CraigScottCapital trending among investors?

It is trending due to online discussions, ads, and curiosity about its investment opportunities.

Conclusion

Financeville CraigScottCapital is a platform that creates both interest and concern among investors. Some people see it as an opportunity, while others question its credibility. This mixed response makes it important to stay alert. Investors should never rely on promises alone.

A careful and informed approach is always the best choice in such cases. Always check facts, reviews, and official details before investing. Taking time to research can help you avoid unnecessary risks. Smart decisions can protect your money and future.

Rehan is an experienced content writer at fitsname.com, specializing in name-related topics. He creates well-researched, creative, and easy-to-understand content focused on animal names, team names, group names, and unique naming ideas. With a strong passion for words and SEO-friendly writing, Rehan helps readers discover meaningful, catchy, and memorable names for every purpose. His goal is to make name selection simple, fun, and inspiring for everyone.